When I started out in my working career I’ve always thought very intentionally about retirement. You know, that mythical creature we’d all hope to reach by the ripe ole age of 65!! I might look something like the picture above (PS – Thx Snapchat Filter)

I began as most do, with an employer sponsored 401K and began socking away money for a day that “could be” 40+ years from when I started. Initial learnings of OPM (Other People’s Money) became apparent as my contribution was “matched” by my employer. I supplemented this work 401K plan with a ROTH IRA contribution. Post tax dollars invested for a similar “someday” but these dollars would not be taxed as they grew or when they would be redeemed. Decent start for someone early in their 20’s…or so I thought.

All that seemingly remained to accomplish my goal of retirement would be to:

- Continue to grow earnings & investing with consistency over time

- Reduce expenses and debt (this almost always makes sense)

- Hope the market continued to grow as it had the last 90+ years

- Don’t die…

Don’t Die?

Killer Strategy (no pun intended!). When saving for “Someday” the importance of don’t die took on a new light when I got into my 30’s and continued growing personal income. I began to question the ideals behind saving and investing (buy, hold, pray) during the best years of my life, so I could retire somewhere in Florida to ease my arthritis and work on my shuffleboard game in my 70’s at a measurably slower pace of life.

The goal isn’t to stash away money for 40-50 years so that some day when I’m 75 and have limited mobility I can be as free as a bird (from expenses). It takes too long!!! What if I wanted to retire 10 or even 20 years sooner? How could that happen?

Mindset Shift

Through an introduction of some terrific business friends, I read, listened to and re-listened to The 4-Hour Work Week, by Tim Ferriss. The “new rich” as he’d described saw retirement not as the end goal, but more a means of being throughout life. Scheduled “mini-retirements” were necessary to live life to the fullest now vs. saving it all for a future someday (the end). This began my learning journey of my 30’s.

Concepts like: Business Ownership, Monthly Cash Flow, Time Management and Target Monthly Income (TMI) became common place in my retirement planning while learning from the “new rich.”

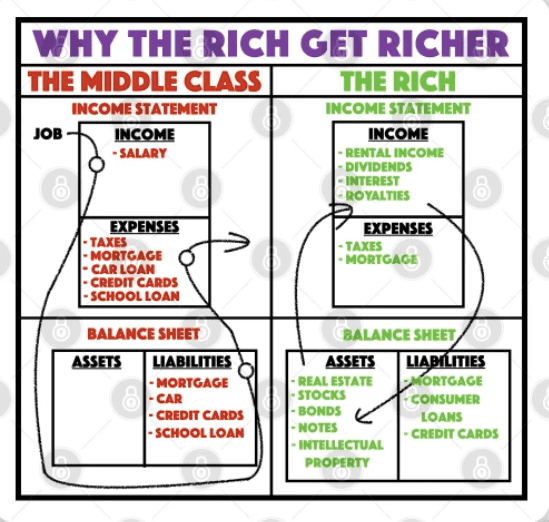

The Rich Don’t Work for Money

I dove back into the classic Rich Dad Poor Dad and the classic teaching from Robert Kiyosaki. I started asking simple questions of the wealthy. How did they get there? What do they do? More importantly…what do they OWN?

Assets like a 401K, IRA, or Roth IRA weren’t accessible until 59 1/2 years old (without substantial early withdrawal penalty) and they’re subject to high tax. As I grew in my knowledge, I also became more aware of taxes on the impact of wealth creation and wealth preservation. Would taxes likely be higher 30 years from now….I’d venture a strong HELL YEAH, at this one!

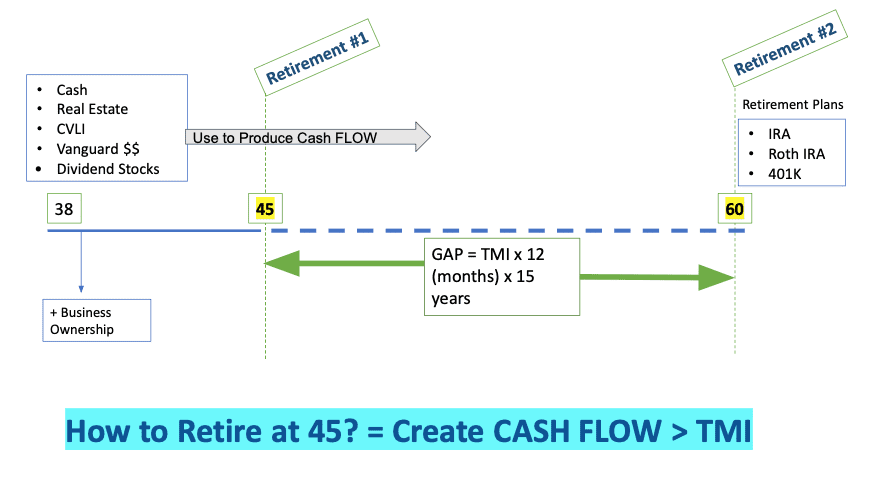

I’m an incredibly visual person and so at 38I drafted this visual to unlock the answer to the question,

“What would it take to retire at 45?”

What would it take to require at 45?

Pretty simple answer. Produce monthly cash flow from investments that exceeds > current expenses. Period. End of story. Invest in assets which produce cash flow. [From: Rich Dad Poor Dad]

There’s a critically important point to make here. I’m 99% sure I won’t retire at 45 to a john boat, weekly fishing expeditions, morning coffee with the boys, and afternoon golf (daily). But, that doesn’t sound too shabby does it?

Back in 2013 I started what I call “Dream Bucket 2027” which is my plan to freedom at 45 years old. I sometimes interchangeably call this mission the “Freedom Fund” as I’m talking about it and investing in assets.

Familiar with the F.I.R.E. Movement?

Financial Independence Retire Early. If you’re not familiar with Mr. Money Mustache, this would be a good side track for you and another POV on early retirement if that’s the mission you’re on. His “mustachian” philosophy is that of aggressive saving and passive index fund investment and aggressively limiting and/or eliminating expenses for financial freedom. Different path, but similar destination in mind.

Where do we go from here?

Today I continue investing in cash flowing assets (primarily real estate) and I feel well positioned given the recent explosion of inflation. I’m also doing a great deal of learning about TAXES and how the wealthy navigate this space (legally)to keep more of what they earn. If you’re wondering why the wealthy don’t pay taxes, consult the IRS Tax code. The tax code is simply a series of “incentives” from the government. The wealthy understand how to use the code. Tom Wheelwright does a terrific job with his TAX FREE WEALTH books and content on this subject.

Nothing Happens without Income Growth

I’m certain there are differing opinions here, but I’ll make this very simple. The first step to any retirement or freedom journey is to MASSIVELY increase your income. A person can live very comfortably and with large steps forward with their income many options will become available. I recommend following Grant Cardone for income explosion inspiration and concepts. I’ve read a few of his books and they’ve been helpful on my journey.

As I move from my 30s to my 40s in 2022, I look back at all the learning I had in my 30’s and how different it was from the learnings of my 20’s. I’m looking forward to further mindset shifts in my journey and I look forward to updating the readers on my DREAM BUCKET journey.